Award-winning PDF software

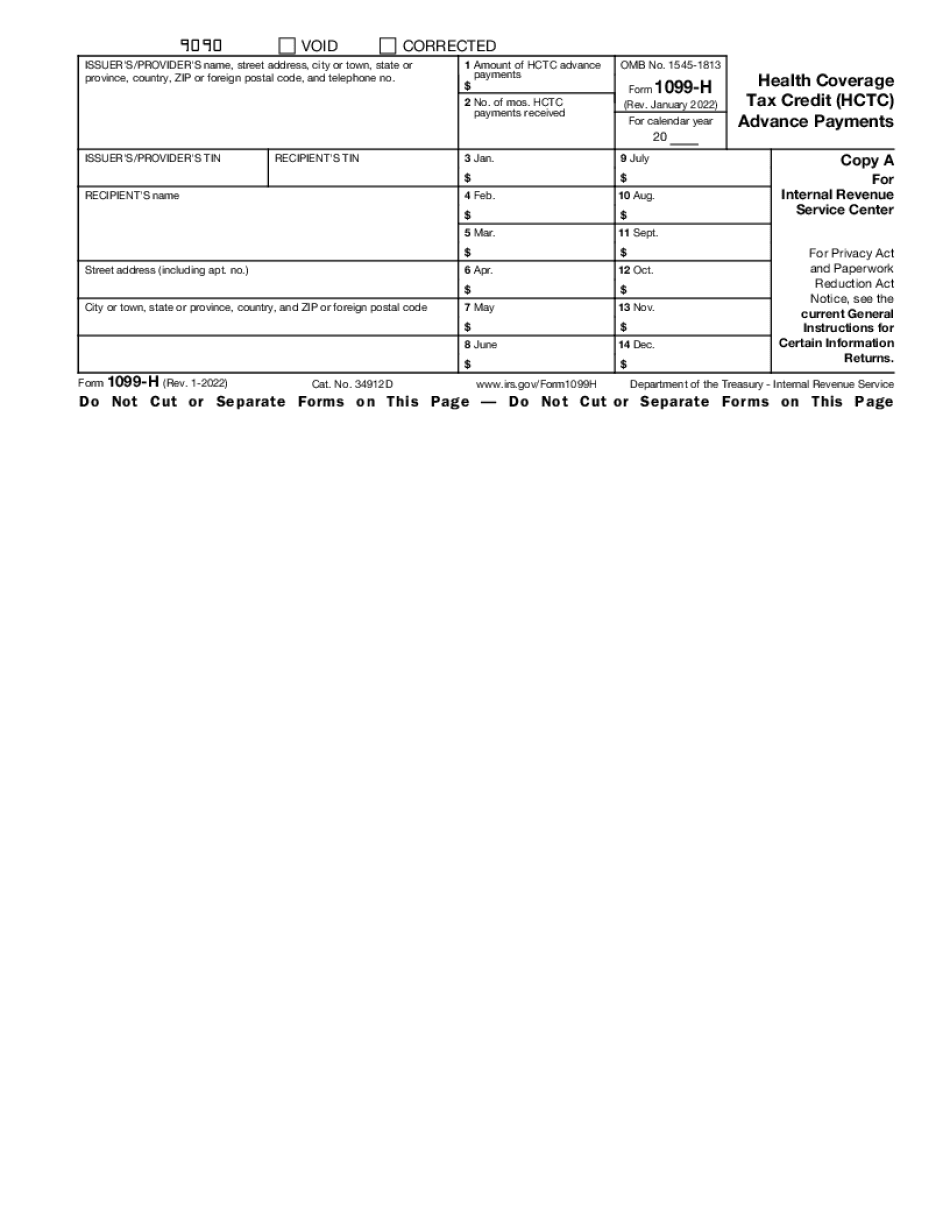

Printable Form 1099-H Vallejo California: What You Should Know

See FTF-120-01) FICA The Social Security tax is collected by a program administered by the Social Security Administration as it is now known. The Tax Court in Philadelphia, PA, has ruled that there is no statutory right or obligation by the employer under sections 6012(a) and 6013 to collect these taxes from the employee. The employer may still be liable under various provisions of the Internal Revenue Code, but this liability is generally limited to those years in which the employee is not entitled to the full amount of Social Security retirement benefits. This limitation is based on two factors. First, a period of continuous service for at least 1 year is required to ensure that the employee will receive the full amount of Social Security. Second, the fact that the employee is an employee is a factor in determining the employee's entitlement to the full amount of Social Security benefits and will, therefore, generally constitute “continuous service.” The Supreme Court has ruled that the employee's entitlement to such benefits does not automatically include the employer's obligation to collect the employer's share of FICA on behalf of the employee. This decision has held that if the employer were required to collect such taxes, for example from individuals who receive Social Security benefits, the employer could not be liable for them under section 62 of the Internal Revenue Code. However, it has held that it may still be liable if the employee does not receive retirement benefits, but is receiving unemployment compensation benefits for the full number of years of service as required by section 501(c)(19) of the Internal Revenue Code. The Supreme Court has specifically held that section 601(c)(19) must apply retroactively when a period of service for at least 1 year has expired. Section 6013 and 6014 — Social Security — FICA Section 6013 governs the employer's duty to withhold social security taxes on behalf of the employee. This section prohibits such withholding from tax-exemption social security benefits except for the following two exceptions. First, the employer may withhold social security taxes from the employees' wages if it “reasonably believes” such taxes are not required to be withheld on behalf of any other employee. Second, if the employer must withhold for any other employee, the company may withhold from the employees' wages only the taxes required to be paid directly by the employer as determined by the Social Security Administration.

Online methods assist you to arrange your doc management and supercharge the productiveness within your workflow. Go along with the short guideline to be able to complete Printable Form 1099-H Vallejo California, keep away from glitches and furnish it inside a timely method:

How to complete a Printable Form 1099-H Vallejo California?

- On the web site along with the sort, click Commence Now and go to your editor.

- Use the clues to complete the suitable fields.

- Include your personal info and contact data.

- Make certainly that you simply enter right knowledge and numbers in ideal fields.

- Carefully verify the articles from the type in addition as grammar and spelling.

- Refer to aid portion for those who have any queries or tackle our Assistance team.

- Put an digital signature on your Printable Form 1099-H Vallejo California aided by the enable of Indicator Instrument.

- Once the form is completed, push Finished.

- Distribute the all set variety by means of e-mail or fax, print it out or help save on the product.

PDF editor allows you to make adjustments with your Printable Form 1099-H Vallejo California from any world-wide-web connected equipment, personalize it in line with your requirements, indication it electronically and distribute in several methods.